Photo: AppHarvest, Somerset Kentucky

The U.S. controlled environment agriculture (CEA) industry received lots of publicity over the past 10 years. From interviews on CNBC to articles in Forbes, investors and the general business community found interest in an industry that seemed new despite the fact that it was anything but.

(If you are interested in the definition of and more information on the controlled environment agriculture and the indoor ag tech industry, please click here.)

This new interest led to substantial capital invested into greenhouses, vertical farms, and other companies supporting the commercial ag-tech and horticulture industry. All this “noise” made it hard to discern what was real, hype or fabricated by overly creative (yet inspiring) pitch decks.

From this point forward, we must focus on a reset of known information. One that clarifies the reality of our U.S.-based commercial food producing horticulture market. This reset must take into account the benefits of all the money invested between 2017-2022 that led to building new farms.

More importantly, it must encourage people, investors and business innovators to continue focusing on the benefits (mostly to growers or farmers) of our small but still-growing controlled environment agriculture industry.

Note: The following information mentions ornamental and cannabis production because these segments contribute to our industry. However, they are not often included in the definition of controlled environment agriculture, indoor ag or vertical farming.

Industry Realities

Let us start with a handful of observations that you are free to comment on below. We will do our best to respond as quickly as possible.

1) The cannabis industry began its path to legalization in 1996 when California legalized medical marijuana. Since then, 40 states followed California in legalizing medicinal use. But the real industry boom began in 2012 when Colorado and Washington legalized recreational use of cannabis.

As of June 2023, 23 states have legalized adult cannabis use. This rapid growth impacted all commercial horticulture because growing cannabis uses the same inputs as all other crops. As such, the industry saw a drastic uptick in the sale of greenhouses, horticulture equipment, irrigation equipment, horticultural lighting and crop consumables (i.e., fertilizers, substrates and pest management products).

The industry also saw massive expansion of companies providing wholesale supply, as well as new horticultural tech companies growing quickly with higher-than-normal profit margins.

- Overly high profit margins on the supply side were due to extremely high profits made by cannabis farmers. This happened because of a few key issues that we likely will not see again. The first was rapid farm expansion due to a race to be first in the market. Second is the semi-legal or illegal status of many farms, which always leads to high profits. And, finally, an emerging market was learning how to be commercial. Early-stage investors saw get-rich opportunities and spent almost anything to move their project to the front of the line.

- The total acreage of legal cannabis production in the U.S. is small compared to commercial ornamental and food crops. In 2021, the average size of a commercial cannabis production operation was 33,900 ft squared (or about ¾ of an acre.)

- As more states legalize cannabis production, the increased volume of legally available weed continues to drive down the price per pound. As this price decreases, ag-tech equipment and supply companies also feel the pinch as operators become more aware of what they’re buying. (I am sure this makes perfect sense to anyone involved in agriculture. A perishable product’s price drops as availability increases.)

2) U.S. interest in vertical farming exploded in the mid-2000s. This was due in part to investment in and formation of Aerofarms in 2004; Dickson Despommier’s 2008 lectures and 2010 book; and numerous inspirational articles, architectural images, and stories from countries concerned with food safety and security. (See the Japan earthquake and tsunami of 2011.)

- All this (plus much more) inspired entrepreneurs, engineers, and technologists with little to no commercial agriculture experience to create business concepts and then pitch them to investors.

- Many of these pitch decks were based on successful Silicon Valley start-up business models that, to date, have struggled in the commercial horticulture and agriculture spaces.

- The investor market was blindly hungry for these ideas. The timing was perfect. At the same time, macroeconomic and political discussions were happening around the world. In 2004, the term “ESG” (environmental, social and corporate governance) was coined and used in a joint initiative led by the United Nations and 20 financial institutions. This report was titled “Who Cares Wins.” The financial industry believed investing in companies that embodied this strategy would win. After all, it would create resilient companies that contribute to sustainable developments, while strengthening the position of the stakeholder and bank. Not long after this, we started hearing thought leaders ask, “How are we going to feed 10 billion people by 2050?”

3) The Netherlands Increased marketing and the promotion of venlo-style, Dutch-designed glass greenhouses as a proven and safe investment for growing select fresh produce. This coupled with early semi-automated leafy green production systems and unique placement of rooftop greenhouses (see Gotham Greens/Whole Foods partnership in 2013), plus the early failures of multiple vertical farms, led to the next round of investments.

- The Dutch horticulture industry was initially left out of the big spending. While they have a long history in horticulture production, the new concepts, crops and money were focused on growing in a unique way. By 2015-2017, the Dutch industry knew they had to be more involved and worked together to improve their market position and awareness. By 2020, leading Dutch companies and Wageningen University Research (WUR) published a report comparing four cultivation methods. Using their interpretation of Sustainable Development Goals (SDGs as defined by the United Nations), it was determined (and then heavily marketed) that “high-tech greenhouses with soilless cultivation, where recirculation of drain water is obligatory, substantially contribute to achieving SDGs.” Read the full WUR 2021 report here.

- Many of these systems did not live up to their marketing claims. Companies did not have the experience to work with or provide guidance on localized issues such as crops, weather (not climate), labor and after-sales service.

- It takes many years to develop crop expertise in each system and for a labor team to come together and operate a growing system that produces the highest possible yields. When done at commercial scales, no proven technologies allow a farm to shortcut these realities.

4) Controlled environment agriculture went “public” and investment firms stepped up with BIG capital. This sparked big interest and even bigger promises from companies looking to get a piece of the money pie. From greenhouse operators such as AppHarvest and Local Bounti, to supply companies such as Scotts Miracle-Gro (owner of Hawthorne Gardening Company) and Hydrofarm, to investment firms such as Equilibrium Capital, COFRA Holdings and Cox Enterprises, the dollars invested in the industry raised to levels never seen before. We all know that when significant dollars get injected into a market, it often leads to “boom” level interest. (See David Chen’s 2021 comments.)

- Many people are responsible for making this happen. From traditional banks facilitating the IPO to recognizable investors to famous personalities, these large investments and public offerings did not happen because a couple farmers decided to take their proven farm public. They happened because of good old-fashioned capitalism and marketing. They happened because people can be inspired by good storytellers. They happened because the financial markets were ripe for such a move.

5) Cheap, abundant capital along with over-promising suppliers and so-called expert consultants chasing dollars led to a boom-industry mentality.

- Interest rates in the 2010s through the early 2020’s were at historical lows.

- There was (and is) lots of cash available looking for annual returns of 10-15%. (In other words, lots of rich people were and are looking for passive income.)

- The pandemic helped the situation due to significant amounts of capital injected into the economy. From retail cannabis sales to garden centers to grocery stores, this cash created a boom for everyone in the supply chain that supported these markets.

A brief history of CEA fresh produce production and greenhouse tomato example

In 2005, UC Berkeley professors Roberta Cook and Linda Calvin published a paper titled, Greenhouse Tomatoes Change the Dynamics of the North American Fresh Tomato Industry. For purposes of this discussion, we will use this paper as a foundation to define industry growth. Reason being, many of the largest investments went into companies that were farms based on assumptions gained from years of CEA industry data.

The reality of this data is that prior to 2010, most of it was based on producing greenhouse tomatoes. Historically, this was a high cap-ex industry with low profit margins that relied on careful cost control, operational excellence, high yields and old-fashioned luck.

The above paper also correctly defines the market as a North American one since the product produced in these facilities competes directly with their field-grown competitors for sales and shelf space. It also stated that U.S.-based greenhouses will be forced to compete with products grown in Canada and Mexico.

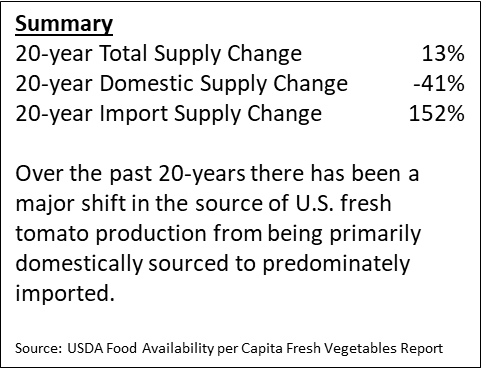

All this remains true today (regardless of crops grown). In 2003, about 1,630 acres of greenhouse tomatoes were grown in the U.S. Twenty years later, our data shows a 20-30% drop in this figure. What changed during this time is the number of crops grown at a larger scale. The addition of more peppers, cucumbers, strawberries, leafy greens, and culinary herbs means that the greenhouse production area has increased to about 2,150 acres.

This means that even with all the money spent over the past decade, our production area only increased about 20-30%. It is also important to note that we are not considering the metric tons produced on these acres. Yield improvements of about 20-40% (depending on crop) have been seen over the past 20 years.

The take home message should be, Americans are consuming more tomatoes. American retailers are just importing more and more of them each year. Even the ones we grow in a greenhouse.

Greenhouse Grower recently released an article showing their account of the largest greenhouse vegetable growers. While we think this is a good start, our data shows their information is slightly understated, somewhat incorrect and easy to misinterpret.

We estimate that the USA CEA production area by acres is +/- 2200 acres. We are excluding vertical farms due to lack of data. And we do not count structures that do not have 4 walls, a door and some means of mechanically managing the environment. This means we do not count hoop houses, but we acknowledge there are many successful farmers using hoop houses to profitably produce crops across the USA.

Why all this matters

For companies such as Urban Ag News, we are built on the hopes that our U.S.-based controlled environment agriculture industry is sustainable and capable of continued growth. Our data indicates that we still have work to do before we can be considered an independent industry. (We depend on the global commercial horticulture industry, including the ornamental and cannabis industries, to be viable.)

Additionally, the data shows that ag-tech investments face fundamental problems. (See Agfunder Report and state of CEA investments in this article in Produce Blue Book as well as one can download this Pitchbook Report.) To understand these problems, consider Professor Michael Porter’s work on competitive strategy. He states that for an investment to be justified, you need a big enough market — and the portion of that market you can access is where you make your profits. So, for instance, if you produce ag technology only suitable for a small area of production, it is unlikely that you will gain a profitable return.

Remember how in 2003 the data showed 1,630 acres of greenhouse tomato production in the U.S.?. In 2022, only about 1,250 acres of tomatoes were produced in greenhouses. In 2003, four large greenhouse operators controlled 67% of the production acres. In 2022, eight large greenhouse operators controlled 80% of the production acres.

There is significant dependence on a few clients who control most of the acreage for ag-tech companies focused on the U.S. market. This means new ag-tech companies must be accepted by nearly all the commercial greenhouses to be viable.

If the technology targets leafy greens and culinary herbs, then it is important to realize that the 2023 industry is even smaller (just under 400 acres). In addition, the leafy greens industry is further challenged by the fact that most players use different production methods, making it harder to find similarities among farms.

All of this means that true ag-tech companies must be ready and willing to explore new geographies that have similar existing markets, target new crops, or focus on more general technology. The easiest are Mexico and Canada in terms of travel. The hardest is Europe. But do not expect them to accept new ideas quickly, as there are just as many local companies competing for business.

The same competitive strategy applies to greenhouse operators and producers as well. The market is highly competitive and as the data shows, much of that competition is coming from Mexico, Canada or the open field. Greenhouse businesses must be solving a clearly identifiable problem while providing a value proposition (ie product) that is clearly “better, faster or cheaper” than the product that is already existing on the market.

Successful companies need capital, time, people and patience. Dutch companies invest heavily to access U.S. markets. Same goes for horticulture companies from Mexico, Canada, Israel, Spain, China, Sri Lanka and any other areas that can produce horticulture technology, supply, consumables and (yes) fresh produce.

We Must Know to Grow

While some might read this article and see it all as doom and gloom, we do not. As stated earlier, we see it as important information to know and understand, so we can accept a reset. Our industry still has tremendous upside.

For the industry to reach its potential, we must understand the following before we can grow:

1) With rising interest rates and increased company failures being announced, investment dollars are harder to come by. We must keep those dollars working and staying in the U.S. (or in your local economy or at least with companies investing in your local industry or economy.)

- If we believe in local, we need to encourage growth within the U.S. (You could make the same argument for any other country and companies looking to build their industry.)

- We know that many of the dollars invested were sent overseas because in excess of 250 acres of greenhouses were built in the U.S. by Dutch greenhouse builders from 2020-2023.

- The more dollars we keep local, the more this money can be used to develop research, education, data and technology that solves problems specific to growing in a local market.

2) We must increase the number of American-led companies “growing” or operating successful commercial horticulture businesses. The current lack of grower or production leadership shows that we do not have the expertise to run these facilities. Keeping dollars in the U.S. should promote the opportunities and education needed to get interested people into the right positions. If we do not do this, then we must change our current political position on immigration and start making it easier to bring in talent from other countries.

- We also need to be honest on our access to labor. It is among the largest costs for any company. Regardless of opinions on tech, we need access to labor in a way that keeps us competitive.

3) Currently, the cost of running U.S. CEA businesses is high because:

- Scalability has not been demonstrated for vertical farms.

- Growers are regional segregated from one another. So supporting businesses have a hard time servicing them as cost-effectively as condensed markets such as the Netherlands or Leamington, Canada.

- Labor costs are high. Local people do not want the jobs and struggle performing the work as effectively as individuals from countries such as Mexico working on visa programs. Unfortunately, visa programs are difficult to navigate, costly and politically unpopular.

- Distribution costs are high and often opaque to the grower depending on the size, scale and distribution or customer relationships the farm has built.

Once we overcome these obstacles, we can and will have a thriving industry. After all, we will still have the same problems we faced when people became excited about our industry.

Traditional farms will continue to be impacted by changing climate patterns and extreme weather events. Fresh produce with little to no pesticides will continue to be sought after by consumers. And we will still need to protect our fresh water sources from nitrogen runoff and agriculture (as well as industrial) contamination.

More about the authors:

Chris Higgins is the chief editor at Urban Ag News as well as the President of Hort Americas. He has been active in the commercial horticulture industry since 1996 and has been focused on controlled environment agriculture since January 2004.

Nathan Farner is the General Manager at Hort Americas. Nathan built his career on helping companies with merger integrations, information technology implementations, business process optimization, and data governance.

All information in this article is property of Urban Ag News, Chris Higgins and Nathan Farner. Any reproduction of this information can only be done with written permission.

Notes: If there is a significant amount of interest in further facts and figures not covered in this article (like more information on legal cannabis market or production area of vertical farms) we will be happy to prepare follow up articles. Please comment on what you want to learn below.

2 Comments

I appreciate your balanced perspective on the challenges and opportunities within the agriculture industry. It’s refreshing to see that you view the information presented not as “doom and gloom” but as a call to action and a chance for growth and improvement. Your points about keeping investment dollars within the U.S. and nurturing local industry and talent are crucial to our leafy green market and the US economy. Emphasizing the need for American-led companies in horticulture is essential for expertise development and ensuring competitiveness. The discussion you raised on the high costs associated with U.S. CEA businesses highlights areas that require attention and innovation, such as scalability, labor access, and distribution efficiency. Addressing these challenges can pave the way for a thriving industry that not only meets the demands of changing consumer preferences but also contributes positively to the environment and local economies. We’re actually working on similar CEA technologies over on our website: https://Freshalternative.farm

We appreciate your response, Ryan! There’s always a chance for growth and improvement. Very cool to see what you’re working on. Keep up the good work!